The Cloud Cost Leaks Hiding in Every PE Portfolio Company

Cloud spend is one of the fastest-growing line items in a mid-market portfolio company's budget. It is also one of the least examined. PE operating teams scrutinize headcount, real estate, and vendor contracts with precision. Cloud infrastructure sits a level down, inside engineering and IT, where the numbers often roll up to a single line in the P&L with no drill-through.

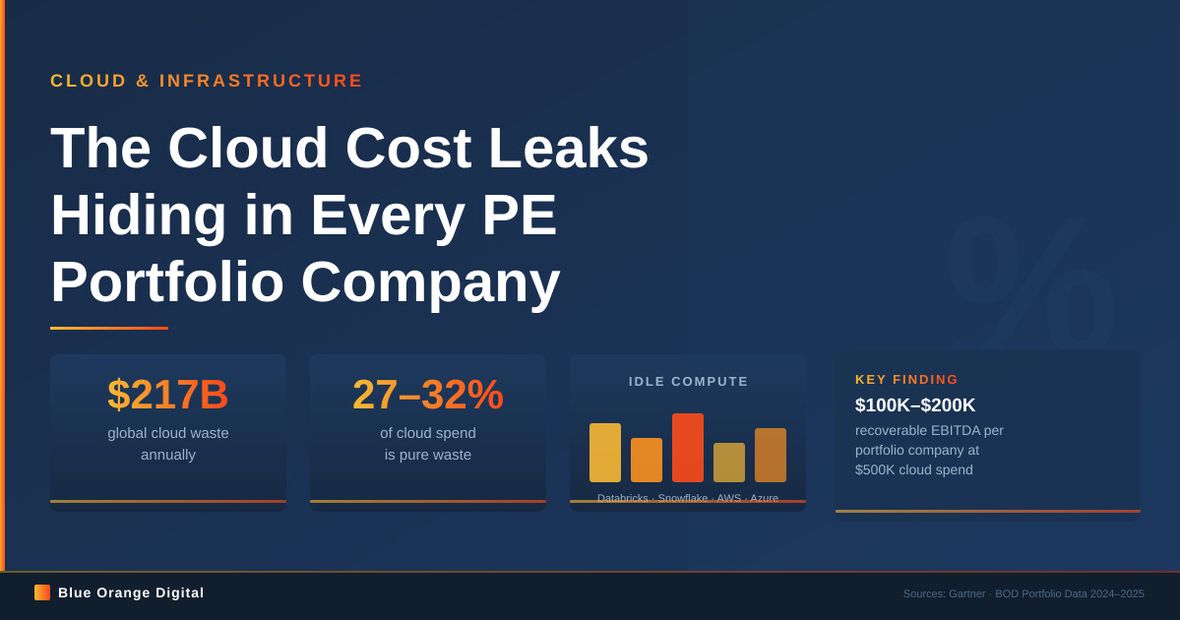

What Blue Orange Digital's data engineers see across hundreds of PE-backed engagements tells a consistent story: between 20 and 40 percent of portfolio company cloud spend is waste. Not optimization opportunity in theory. Actual spend on resources that produce no business value: idle compute running through weekends, warehouses sized for peak loads that never materialize, pipelines duplicated across business units that never spoke to each other, storage that no one queries and no one deletes.

For a portfolio company spending $500,000 a year on cloud infrastructure, that range represents $100,000 to $200,000 in recoverable EBITDA. Across a firm managing eight to twelve portfolio companies, the number compounds.

The Pattern That Repeats

The consistent finding is not that cloud waste is common. It is that it is structural. The same three or four failure modes appear across different industries, different platforms, and different company sizes.

The first is compute that runs when no one is watching. Virtual machines, containers, and analytics clusters that spin up for a batch job or a demo and never come down. At mid-market scale, where a single Databricks all-purpose cluster might cost $80,000 to $120,000 a year, one unchecked cluster is meaningful.

The second is warehouse sizing that never gets revisited. A Snowflake warehouse gets configured for a data migration or a heavy analytics push, provisioned at the XL tier, and stays there. The migration finishes. The analytics team moves on. The warehouse idles at full price.

The third is untagged infrastructure. When a cloud resource carries no cost center, no owner, and no application tag, it cannot be attributed, and what cannot be attributed cannot be managed. Engineering teams that grew fast often have 30 to 40 percent of their cloud spend untagged. No one can tell the CFO what it is for.

The fourth is dev-prod sprawl. Development environments meant to be temporary become permanent. Staging environments built for a launch or a QA cycle stay up at production scale. The infrastructure footprint doubles in ways that never show up in a headcount review.

Why Internal Teams Miss It

The waste persists not because internal teams are inattentive, but because the structural conditions work against finding it.

A cloud team at a portfolio company sees one company's spend. They have no benchmark for what a well-run data platform of their size and complexity should cost. When the Snowflake bill comes in and it looks like it did last month, that looks like stability rather than a signal worth investigating. Without peer data, there is no reference point for "this is abnormal."

The incentive structure compounds the problem. The platform engineering team that built the current architecture has no natural motivation to reduce the scope of what they built. The Databricks or Snowflake account team has a strong interest in expanding usage, not auditing it. Neither party is positioned to tell a CFO that 30 percent of what they are paying for is producing nothing.

Vendor account reviews, the primary feedback mechanism most companies rely on, are designed to surface upsell opportunities and adoption gaps, not cost inefficiency. A Snowflake QBR will show query volume growth and recommend larger warehouse tiers for better performance. It will not flag that three separate business units are running separate, partially overlapping pipelines into the same source tables.

The result is that cloud spend grows quarter over quarter in a way that feels correlated with business growth, when a meaningful portion of that growth is pure structural waste.

Where the Leaks Live on Each Platform

The specific waste patterns vary by platform. Blue Orange's data engineers have mapped them across Databricks, Snowflake, Microsoft Fabric, Azure, and AWS.

On Databricks, the highest-value targets are cluster configuration and job scheduling. All-purpose clusters that should be job clusters. Interactive clusters with no autotermination timeout. Cluster policies that allow engineers to spin up arbitrarily large instances without approval workflows. Jobs scheduled to run on fixed schedules rather than triggered by data arrival, so they run empty when upstream pipelines are delayed. Unity Catalog governance gaps that allow compute to be provisioned outside of cost controls entirely.

On Snowflake, autosuspend configuration is the most common finding. A warehouse set to suspend after ten minutes of inactivity rather than sixty seconds costs roughly ten times what a properly configured warehouse costs for the same workload. Storage is the second lever: Snowflake charges for Time Travel and Fail Safe retention that teams set to maximum values they never need and never reduce. Query efficiency is the third: a single poorly-written query running against a full table scan on a large warehouse can cost more per month than a full-time engineer.

On Azure and AWS, the most common findings are oversized virtual machines that were right-sized for a migration load and never resized after, reserved instance coverage gaps on workloads that are clearly long-term, and S3 or Blob Storage data that no application has read in over a year but continues to generate storage charges.

The cross-platform finding is pipeline duplication. When business units operate independently, they often build separate ingestion pipelines from the same source systems. The same Salesforce or SAP extract runs three times into three different data lakes. Consolidating those pipelines reduces both cloud cost and operational complexity in a single move.

From Finding to Fixed

Cloud cost work that does not move to execution produces a report, not a result. The methodology that Blue Orange brings to portfolio companies starts with a read-only assessment that requires no infrastructure access and no disruption to running systems.

The assessment phase maps current spend by service, by team, and by purpose. It identifies the untagged resources and assigns probable owners. It sizes each waste category in dollars and ranks them by the ratio of potential savings to implementation effort.

Not all savings are equal in that ratio. Turning on autosuspend in Snowflake is a configuration change that takes an hour and recovers $30,000 to $80,000 a year for a typical mid-market deployment. Consolidating three independent data pipelines into a shared ingestion layer is a meaningful engineering project. The sequencing prioritizes the configuration fixes first to generate early wins and cash recovery, then schedules the architectural changes within the broader engineering roadmap.

The execution phase covers the actual changes: cluster policy updates, warehouse configuration, tagging enforcement, pipeline consolidation, and right-sizing. For most mid-market portfolio companies, the full optimization cycle from assessment to implemented changes runs eight to twelve weeks. The savings appear in the next monthly cloud bill.

For a deeper look at how cloud efficiency connects to the diligence process, the forthcoming article in this series covers cloud infrastructure as a formal dimension of pre-acquisition data due diligence.

The Portfolio-Wide Angle

The math looks different when a PE firm applies a cost playbook across a portfolio rather than one company at a time.

A firm with ten portfolio companies that each spend $400,000 a year on cloud infrastructure carries roughly $4 million in aggregate annual cloud spend. If the 20-to-40-percent waste pattern holds across the portfolio, the recoverable range is $800,000 to $1.6 million. Captured in year one of the hold period, that recovery contributes directly to EBITDA at a multiple.

More practically, a firm that has run this playbook once has the audit templates, the benchmarks, and the remediation runbooks ready to apply to the next acquisition. The first engagement builds the playbook. Subsequent engagements run faster and cost less.

The benchmark data also compounds. After running cost assessments across multiple portfolio companies in the same sector, an operating team accumulates real spend-per-workflow, cost-per-query, and infrastructure-to-revenue ratio data that no single company could develop internally. That benchmark data informs both diligence underwriting and post-close planning at a level of specificity that generic industry reports cannot match.

Blue Orange's EDGE program is structured for this model. The portfolio-wide playbook covers three to fifteen companies under a single firm, with outcome-aligned pricing that ties engagement cost to the savings delivered. EDGE includes Assess, Deploy, and Scale phases designed to take a portfolio company from initial assessment to optimized, AI-ready data infrastructure on a defined timeline.

Cost Discipline Now, AI Cost Discipline Next

There is a forward-looking dimension to cloud cost work that sits above the immediate EBITDA recovery.

AI and data compute is repricing. Foundation model providers are moving toward contracted, multi-year capacity commitments rather than elastic on-demand consumption. A portfolio company that spends $2 million a year on cloud infrastructure today may be negotiating capacity contracts for AI inference and training within 18 to 24 months, where per-workflow compute budgets become a hard line in the cost of goods sold rather than an on-demand variable expense.

Portfolio companies that have not done the work to understand, attribute, and control their current cloud spend are not positioned to manage that shift. They do not have the tagging and governance infrastructure to know which workflows consume which compute. They do not have the unit economics to evaluate whether a contracted capacity commitment makes sense against their actual workload patterns.

Cloud cost discipline now is the foundation for AI cost discipline in the next planning cycle. The companies that get this right in 2025 and 2026 are the ones that will be able to treat AI compute as a managed business input rather than an uncontrolled expense line when that transition arrives.

Cost discipline is also one of the prerequisites examined in Blueprint's AI readiness assessment. The connection runs in both directions: companies that cannot explain their current cloud spend are not ready to commit to AI compute contracts.

Where to Start

For a PE operating partner or a portfolio company CFO approaching this for the first time, the practical starting point is not a full audit. It is a structured assessment that produces a prioritized list of findings with dollar values attached.

Blueprint's assessment is read-only, takes ten minutes, requires no infrastructure access, and benchmarks the company's data and cloud infrastructure against peers. It surfaces the structural waste patterns and sizes them, so the operating team can decide which remediation to prioritize without committing to a full engagement upfront. Results come back as an immediate PDF.

The 20-to-40-percent waste finding is not a forecast. It is what Blue Orange's data engineers see when they look at a mid-market portfolio company's cloud spend with a methodology designed to find it. The question is whether it is worth ten minutes to find out where your portfolio companies stand.

Run the Blueprint assessment to surface the leaks in your portfolio company's cloud spend.