When a board pushes a portco management team on AI, the first thing that usually happens is a flurry of pilot announcements. The second thing is a self-assessment that lands one level higher than reality.

I've seen this across enough due-diligence engagements and value-creation projects at Blue Orange to put a framework around it. We use an enterprise AI maturity model with five levels, L1 through L5. The point of the model is simple: the level you operate at is a diagnosable fact, not a self-assessment. And the fact is almost always lower than what the board deck claims.

Why Self-Assessment Runs a Level Hot

A few copilots feel like progress. A team has a ChatGPT integration, engineers on Cursor or Claude Code, a vendor demo that impressed the operating partner. So when someone asks how mature the AI is, the honest answer is L1, but the instinct is to say L3.

The gap between a few people using copilots and an agent running a workflow end to end is enormous. It is a data, workflow, and orchestration gap, not a model gap. Companies sit on the wrong side of it and don't know it, partly because the model layer has become impressive enough to demo well no matter what sits underneath.

Naming the level you actually operate at, and naming the one thing blocking the next level, is where the work starts.

The Five Levels of the AI Maturity Curve

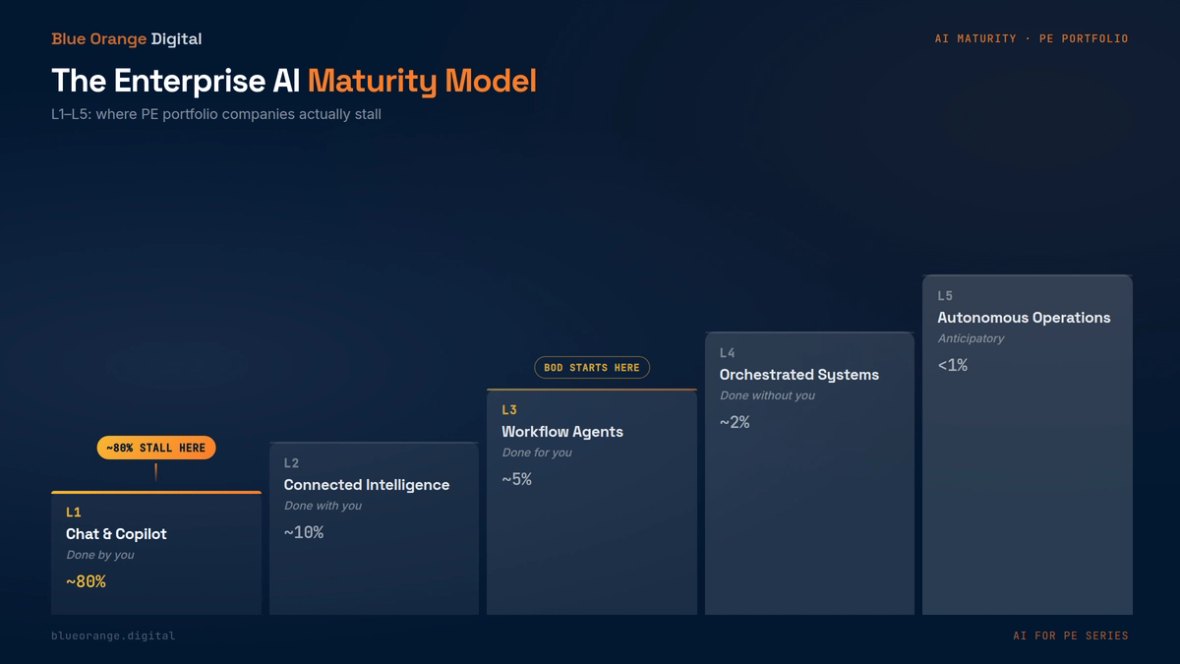

Here is the AI maturity curve we use, and roughly where the middle market sits on it.

L1: Chat and Copilot. Done by you. A person prompts, edits, and decides. Real per-seat productivity, no process redesigned. The orchestrator is the human. Around 80% of the mid-market is here, and most of it stalls here.

L2: Connected Intelligence. Done with you. The model is grounded in your own data through retrieval, so answers are cited and trustworthy instead of generic. The orchestrator is still the human. This is where most AI ROI stories actually live, and roughly 10% of companies have reached it.

L3: Workflow Agents. Done for you. An agent runs a multi-step workflow on its own, and a human reviews the result. The orchestrator becomes the workflow, and cost per task replaces cost per seat. About 5% of companies operate here.

L4: Orchestrated Systems. Done without you. Specialized agents coordinate through shared state and a control plane, running durably across hours or days. The orchestrator is the agent, bounded by policy. Roughly 2% of companies are here.

L5: Autonomous Operations. The system works like a colleague, with durable memory of the business, initiating work instead of waiting to be asked. It is the frontier, real today only in narrow domains, and under 1% of companies touch it.

The Bottleneck Is Rarely the Model

The maturity curve makes one thing explicit: the constraint at the lower levels has almost nothing to do with which foundation model you are using.

An L1 company that buys a better enterprise AI license is still an L1 company six months later. Swapping one frontier model for another does not change the fact that nobody redesigned a process. The bottleneck is that a new analyst cannot get clean data without a Slack favor, and no model resolves that.

An L2 company where two teams produce different revenue numbers for the same quarter has a trust problem that predates any AI system. Models run on inconsistent data produce inconsistent outputs. The vendor cannot fix your data pipeline.

At Blue Orange, the most common failure pattern we see in portco AI engagements is reaching for a better model when the move is to fix the layer below or redesign the workflow above. That is harder to sell internally because it looks like infrastructure work rather than AI work. For any company below L4, that distinction is artificial.

Stop Climbing the Stack. Start Where the Economics Are.

The standard industry story tells portfolio companies to start at L1, build to L2, hope to reach L3, and dream of L4. That story keeps the systems integrator employed. It does not deliver EBITDA.

We invert it. We start at L3, because L3 is where the economics show up. A per-seat productivity bump at L1 is worth tens of basis points of EBITDA. A workflow an agent runs end to end at L3 and above is worth hundreds. So we anchor on the single highest-ROI workflow, ship it production-grade in about 90 days, and prove the economics before scaling.

From that anchor we move in both directions. Down into the L2 data substrate, as the agent's grounding needs surface. Up into L4 orchestration, as the workflow earns it. And we put L1 humans back at the escalation edge, as the exception handler, not the default operator. The 80% chat-and-copilot adoption is not the destination. It is the surface area that remains after the workflow is automated.

What This Means on a PE Hold Timeline

Private equity operates on 3 to 5 year holds. That timeline favors compounding over flashy demos, because the EBITDA impact climbs sharply as you move up the levels.

A portco that spends Year 1 standing up one L3 workflow has a repeatable asset that makes every project after it faster and cheaper. A portco that spends Year 1 buying L1 seats has the same demos it had at the start, plus technical debt and a data team that has learned to be skeptical of AI initiatives.

The exit creates a forcing function too. Buyers are asking harder questions about AI in diligence than they were two years ago. The question is no longer whether you have AI. It is which level you actually operate at, whether the data supports it, and whether the team can ship and maintain it without heroics. A company at L3 or L4 answers that cleanly. A company at L1 or L2 is running a demo.

Knowing Which Level You Are At

The enterprise AI maturity model is useful because it names the level you actually operate at right now, and the one bottleneck blocking the next one. For most PE-backed portcos, that constraint is data access, data quality, or a workflow nobody has redesigned. Buying a better model does not move you up a level. Building the layer below it, and automating the workflow above it, does.

If you want a diagnosable read on where a portco sits and which workflow to attack first, that is the core of the work Blue Orange does with PE sponsors and their portfolio companies. Reach out if it would be useful to talk it through.

Most portcos stall in the same predictable places. The Cliffside Chronicle tracks what separates the ones that break through: a curated digest on AI, data, and PE value creation, sent every two to three weeks. Subscribe here.