Most Mid-Market Companies Think They're AI-Ready. Most Aren't.

By Josh Miramant

Here is what I keep seeing in the field.

A CFO at a mid-market industrials company tells me their organization is "actively working on AI." When I ask what that means concretely, they describe a ChatGPT enterprise license, a standing weekly AI committee, and three pilots in various stages of "near completion." No baseline assessment. No score against peers. No way to know whether they're ahead or behind where a company their size should be in 2026.

This is the pattern across nearly every mid-market company I talk to. Leadership knows AI matters. Budgets are moving. Pilots are running. But almost nobody has measured where they actually stand. They've confused activity with readiness, and the distinction is starting to matter in ways that show up in operating results.

That gap between activity and readiness is expensive. And it's getting more expensive every quarter.

The benchmark nobody wants to look at

McKinsey surveyed roughly 2,000 organizations on AI adoption. Only about 6% cleared the bar of significant AI value: measurable improvements that translate to a 5% or greater EBIT impact. The companies that made it were three times more likely to have fundamentally redesigned their workflows, not just layered AI tools on top of existing processes.

Six percent.

The other 94% are running pilots, signing licenses, and attending conferences. They are generating activity but not outcomes. And most of them do not know which category they're in, because they have never measured.

That is the core problem with how mid-market companies approach AI right now. They're making decisions without a baseline. They're comparing themselves to industry narratives instead of actual peer data. When the question comes from the board or from a PE operating partner during a value-creation review, the honest answer is: we do not know where we stand.

What AI readiness actually means

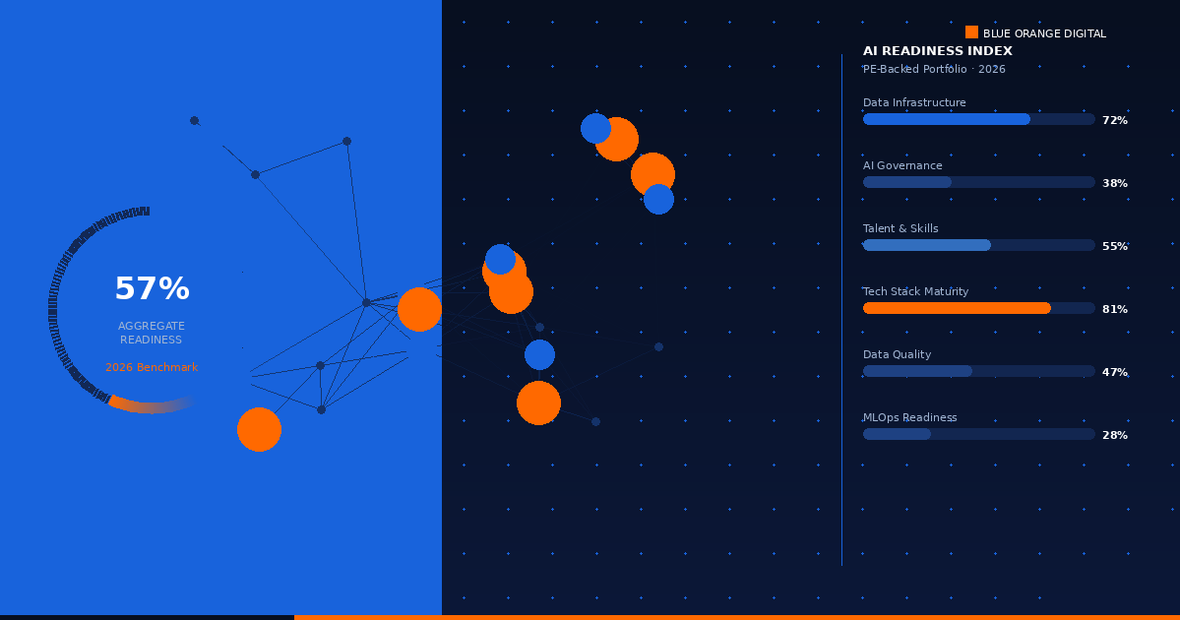

The term gets used loosely, so let me be specific. AI readiness is not about which models you've tried or how many people attended a prompt engineering workshop. It breaks down into four concrete dimensions. Most organizations have real gaps in at least two of them.

Data infrastructure is the foundation. Can your data be trusted? Is it clean, documented, and accessible to the systems that would consume it? A company with a year of operational data spread across five disconnected source systems is not data-ready, no matter what AI tools they've purchased. Most mid-market companies built their data architecture to support reporting, not AI consumption. That architecture needs to be assessed before any serious deployment starts. In our experience, this is the dimension where organizations are farthest from where they think they are.

Workflow design is where most organizations underestimate the problem. Putting an AI tool on top of a broken process makes the broken process faster, not better. The companies generating real returns from AI have gone back and redesigned the workflow first, then deployed AI into the redesigned version. That is a more deliberate investment. It takes longer, requires more organizational discipline, and produces meaningfully better results. Most companies are not there yet. They are optimizing the old process, not replacing it.

Governance is the area with the most denial. Governance means having clear policies on who can use AI for what, how AI-generated outputs get reviewed before they inform decisions, and how you actually measure whether AI is producing the results you expected. Most organizations have none of this in writing. Some have informal norms. Almost none have a measurement framework. That is a liability as models become more capable and more embedded in operations that touch customers, finances, or compliance. When an AI system is producing confident-looking output with no review gate, and nobody owns the question of whether that output is actually correct, that is not a theoretical risk.

Organizational capability is the most human dimension. Does your leadership understand AI well enough to direct it, not just sponsor it? Do you have named people whose actual job includes making specific AI workflows production-ready, not as a side project, but as a primary accountability? Not a committee that meets biweekly. Named individuals with specific deliverables, a budget, and a timeline. Most mid-market companies are still in the committee phase. That phase does not produce outcomes.

The score gap

These four dimensions are measurable. You can score a company on each one, aggregate those scores into a readiness profile, and compare that profile against companies of similar size, industry, and growth stage.

That comparison is the part that matters most.

The question every executive should be asking is not "are we doing AI?" That question is almost always yes. The question is: "compared to similar companies, where do we actually stand, and where are the specific gaps that carry the most risk or the most near-term opportunity?"

Without a benchmark, AI strategy becomes opinion. With one, it becomes a roadmap.

This is what we built Blueprint to do. Blueprint gives mid-market executives a structured AI readiness assessment across these four dimensions, compares results against a relevant peer set, and surfaces the specific gaps with the biggest operational impact. Not a 60-page consulting report. A score you can actually work from.

The companies running through Blueprint are finding a consistent pattern: data infrastructure is further along than expected, while governance and organizational capability are significantly further behind. That finding is useful. It tells you where to direct the next quarter and where a vague "we're working on AI" answer will eventually catch up with you.

Why this matters right now

The window for getting ahead of this is narrowing. Two years ago, being AI-curious was enough to differentiate at the executive level. Today, companies in your vertical have moved past that. Some have redesigned workflows. Some have agents running in production. Some are seeing real margin improvement from AI, not just cost savings on individual tasks.

PE sponsors now expect to see an AI plan in the investment committee memo. In conversations I've had with operating partners this year, AI deployment capacity comes up in almost every IC discussion. Several have told me it now accounts for somewhere between 30 and 40 percent of the meeting.

The 6% who are generating meaningful value did not get there by running more pilots. They got there by knowing where they stood, making specific decisions about where to invest, and holding someone accountable for the result.

Knowing your score does not mean you have solved the problem. It means you know what you are actually working with. That is the starting point for everything else.

Take the Blueprint assessment to see where your company stands relative to peers: blueprint.blueorange.digital